Lumentum Is Starting Its Second Engine

From $88 to $1,085, and What a 25% Drawdown From the Peak Really Means

A tenfold gain and a 25% loss. Two opposite numbers attach themselves to the same stock at the same time. A name that went from $88 to $1,085 in a year now sits 25% below its high. Some call it a stock that more than 10x’d in twelve months. Others call it a stock that has fallen a quarter from its peak. The fact that one company can carry two such opposing narratives at once is itself a compact summary of where Lumentum stands today.

Has the market already priced Lumentum perfectly, or is there something it still hasn’t seen?

If that run-up is already fully reflected in the numbers, then the current pullback is the natural process of froth coming out. If there is still something unaccounted for, this drawdown is a different kind of phase entirely. What separates the two comes down to what this company actually makes money on, and how much of the source of that money is already baked into the price.

This article takes the company apart. Lumentum has drawn attention as the supplier of the next-generation EML that goes into 1.6T optical modules. The market sees the next stop for that EML as jumping straight from 200G to 400G.

But one variable cuts into that picture.

Word on the ground is that Google has asked for 300G in between, a per-lane speed that has never existed before in the history of optical interconnect. Why is 300G being discussed at all, not 400G and not 200G, and if it is real, what does it mean for Lumentum and the optical market? That question is one axis of this piece.

There is a second axis. Even the EML business that holds up the stock today is, by the CEO’s own description, still in its early innings as part of a much bigger picture. This article maps where the line sits between what is already in the price and what is not yet, and how that line changes the way you should look at the current valuation.

If you hold Lumentum or are watching it, this is worth reading as one framework for how to think about the company.

Table of Contents

Two Numbers: A 10x Run and a 25% Drawdown

How the Market Sees Lumentum: Only the 200G EML Monopoly

Re-examining the First Engine: Is 200G Really Followed by 400G?

The Second and Third Engines: OCS, CPO, and Google Scale-Up

The Real Meaning of Nvidia’s $2 Billion: Solving the Capacity Bottleneck Directly

The Other Side of the Bull Case: What Breaks This Picture

How I See the Investment

Disclaimer

This article is an analysis based on publicly available results, company disclosures, and scenarios being discussed in the industry. It does not recommend buying or selling any specific security. The content described here as coming from the ground is not fact confirmed by standard documents or official announcements but rather a direction being talked about in the industry. The company names, supply relationships, and order details that appear in the body are based on public reporting and corporate filings, while the interpretation of figures and the outlook reflect the writer’s own views. Stock prices and financial figures are as of the time of writing and may change afterward. Responsibility for investment decisions and their outcomes rests entirely with the reader.

1. Two Numbers: A 10x Run and a 25% Drawdown

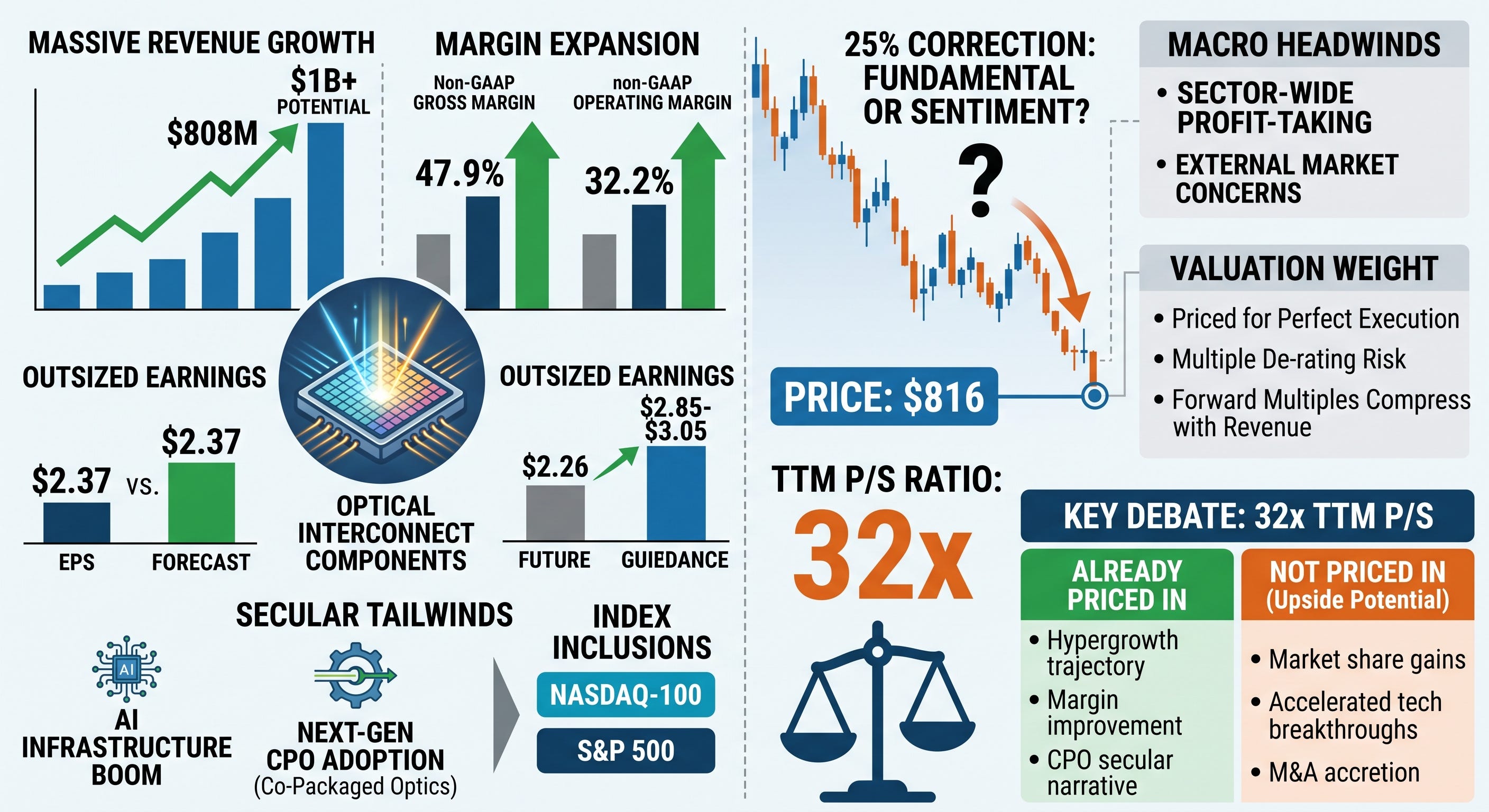

Lumentum’s gains over the past year are not just the result of one earnings surprise. During the rally, the company was added to the Nasdaq-100 and entered the S&P 500. An optical component maker becoming a constituent of large-cap tech indices within a single year tells you something about the nature of this move. It is not the good news of one individual stock. It is the market’s acknowledgment that this company stands at a chokepoint in the enormous flow of capital called AI infrastructure.

So how should the recent 25% correction be read? Is it because the fundamentals have deteriorated, or for some other reason?

Look at the fundamentals first and there is no trace of damage. The company’s most recent quarterly revenue was $808 million, a record high and up 90% from a year earlier. Non-GAAP gross margin was 47.9% and operating margin was 32.2%, a full reversal from the negative operating margin of a year ago. Non-GAAP earnings per share came in at $2.37, above the consensus of $2.26.

More important is the guidance for the next quarter. The company guided next-quarter revenue to $960 million to $1.01 billion. That signals crossing $1 billion in quarterly revenue, with operating margin rising to 35% to 36% and EPS climbing to $2.85 to $3.05. Revenue nearly doubling while margins rise at the same time means this growth is not the kind that fills volume by cutting price.

So why did the stock fall?

One reason is the macro. As profit-taking spread across AI infrastructure broadly, the optical group as a whole got shaken once, and at certain points external variables such as concern over the delayed IPO timeline of a large AI company became the trigger for a selloff. This was not a Lumentum-specific problem but a stretch where the whole sector moved together.

The other reason is the weight of the multiple itself. At a stock price of $816, a market cap of roughly $58 billion divided by trailing twelve-month revenue of $1.8 billion gives a price-to-sales ratio of about 32x. That said, this is a trailing figure calculated on revenue that has already passed, so once the quarterly run rate that has already crossed $800 million enters the denominator, the multiple comes down fast at the same stock price. Even so, 32x already prices in near-perfect execution, and a multiple like that reacts sharply to even small disappointments. Revenue can beat slightly and the stock still falls if it misses the market’s elevated expectations.

So that 32x is the counterweight that anchors this entire article. Throughout the bull case, you cannot lose sight of what this multiple has already pre-priced. At 32x revenue, the figure already absorbs much of the next generation’s pricing premium and the directional move toward CPO beyond it.

What needs to be weighed is not simply whether Lumentum is a good company but, among the paths along which that direction actually lands as revenue, which ones still sit outside that 32x. If there are such paths, the current correction reads differently. If there are not, 32x is just an expensive price.

2. How the Market Sees Lumentum: Only the 200G EML Monopoly

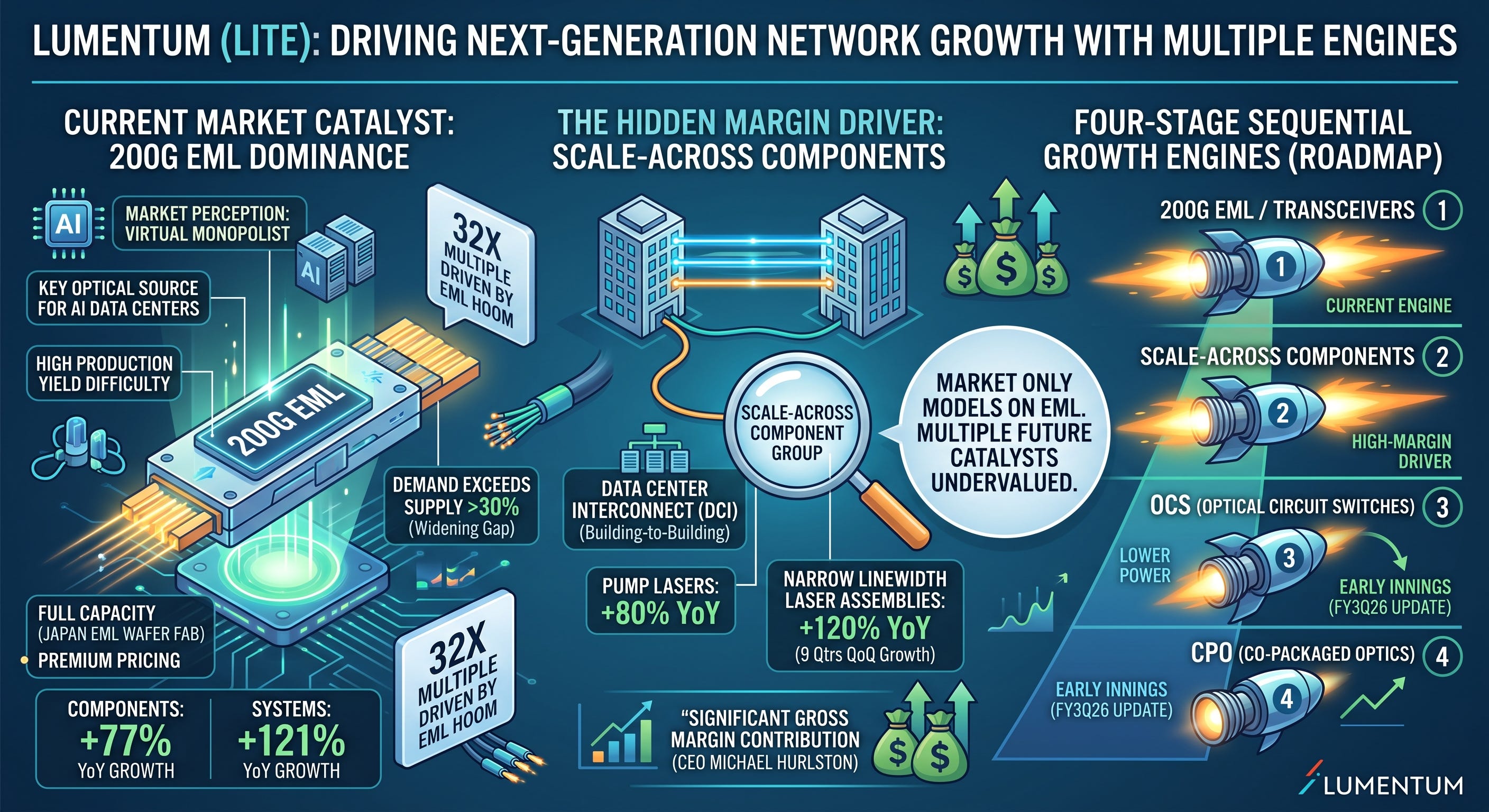

Lumentum splits into two segments. One is Cloud and Networking, which makes the optical components, modules, and subsystems that go into AI data centers and telecom networks. The other is Industrial Tech, which handles industrial lasers used in semiconductor equipment, displays, and battery manufacturing. What has driven the stock is overwhelmingly the former. In the company’s results, revenue is broken into two product lines, Components and Systems, and in the most recent quarter Components reached $533 million, up 77% year over year, while Systems reached $275 million, up 121%. Both are figures pulled up by AI data center demand.

The way the market sees this company boils down to one sentence:

the supplier that effectively monopolizes 200G EML.

The EML (Electro-absorption Modulated Laser) is the core light source inside an optical module that converts electrical signals into light, and the perception is that Lumentum is essentially the only place that can reliably supply this at production yield in the next-generation 200G class.

That perception is backed by numbers. The company stated that demand exceeds supply by more than 30% in EMLs and pump lasers, and CEO Michael Hurlston said that gap actually widened from the prior quarter. The Japanese EML wafer fab is running at full utilization at premium prices and still cannot keep up with demand. This is the textbook situation where the supplier holds pricing power, and it is exactly why margins are jumping.

It is worth flagging another axis that has lifted margins here. That is the scale-across components the company highlighted separately this quarter. If the EML is the light source that creates signals inside the module, scale-across is the group of parts that goes into long-distance connections joining building to building, or distant sites to one another.

Pump lasers and narrow linewidth laser assemblies belong here, and narrow linewidth grew for a ninth straight quarter sequentially, up 120% year over year, while pump lasers grew 80% year over year. Hurlston directly stated that this scale-across receives fewer headlines but contributes substantially to gross margin improvement. While the market reads the margin story as a single line about EMLs, there is one more axis holding up the company’s margins.

Seen this way, the growth drivers Hurlston is sketching come in four strands: transceivers, OCS, CPO, and the scale-across just discussed. And of these four, the only one the market has fully put into the price is, in effect, the first and the EML inside it.

The timelines of these four strands are also all different. At the FY3Q26 results in May 2026, Hurlston named optical circuit switch (OCS) and co-packaged optics (CPO) as growth drivers still in their early innings. He chose that phrasing himself. The 200G EML boom that holds up the 32x multiple today is, from the company’s point of view, the first engine already running, and beside it are more engines that have only just been turned over. While the market models this company on the single axis of EML, the company is sketching several engines whose start times differ.

And starting with the very first engine, the EML, there is a sound coming from the ground. Word is that Google has ordered not 400G but 300G to follow 200G.

Why a 1.5x step that has never existed in the history of optical interconnect is being discussed is something you have to understand to read both Lumentum as an investment and where the optical market goes from here.

We start again from that one point.

Coherent: The Company That Gets Stronger in the CPO Era

A stock that traded at $77 a year ago now sits at $385. In early June it hit an all time high of $440. The one year return is north of 370%. Over that stretch NVIDIA poured $2B directly into the company, it joined the S&P 500 this past March, and its market cap quietly climbed toward $75B. This is the story of Coherent (NYSE: COHR), standing at the center of this year’s optical sector rally.