Beyond NVIDIA and Broadcom: What the Market May Be Missing

Cisco: The Third in Line for AI Infrastructure Re-rating

As of March 26, 2026, the Nasdaq has entered correction territory, the S&P 500 is down about 4% for the month, Brent has moved above $100, and the VIX has remained elevated in the high 20s

One stock has been quietly grinding higher through all of it.

After getting hammered down to the $74 range following a margin shock in its February earnings, Cisco has been steadily recovering while the broader market falls apart. CNBC recently flagged the chart, noting Cisco has a real shot at meaningfully breaking through its prior highs. There's a reason this is happening while everything else is selling off: Cisco sits at the intersection of defensive positioning and AI infrastructure growth, and the market is just starting to figure that out.

Disclaimer

This article does not constitute investment advice, a recommendation, or a solicitation to buy or sell any securities. All investments carry risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.

1. What Cisco Is, and Why Now

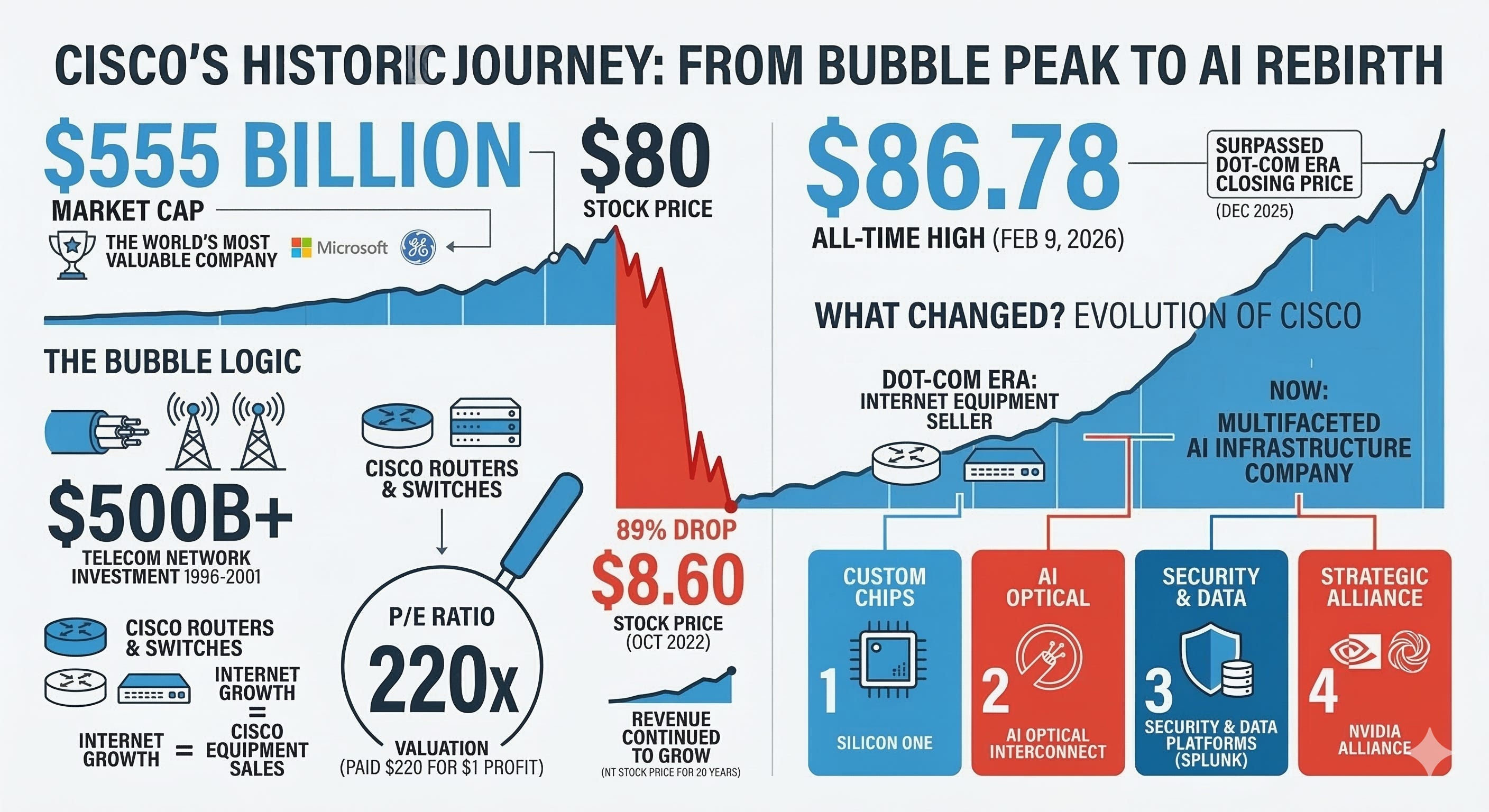

For a long time, the market has thought of Cisco as a relic of the dot-com era. The company that made the routers and switches data had to pass through, holding roughly 75% of the global router market at its peak in the mid-1990s.

In March 2000, Cisco briefly became the most valuable company in the world at around $555B in market cap. The P/E was 220x. Then the bubble burst. The stock fell 89%, from $80 down to $8.60. The company survived, but the stock spent over 20 years never recovering its all-time high.

That same Cisco broke out above its dot-com era closing high in December 2025, 25 years later. On February 9, 2026, it hit an all-time high of $86.78.

What changed?

Silicon One, its internally designed chip.

The Acacia acquisition, which brought coherent optical technology in-house.

A strategic partnership with NVIDIA.

Splunk, which gave Cisco a security and data platform.

Revenue is still anchored in networking, but the Cisco of today is a company trying to own the entire connectivity layer of AI infrastructure.

Two structural shifts are creating the window.

First, the bottleneck in AI infrastructure is migrating from GPUs to the network.

You can stack as many GPUs as you want. If the fabric connecting them can’t keep up, the whole system gets throttled. Running a 128,000-GPU cluster requires three layers of high-speed interconnect: scale up within the rack, scale out between racks, and scale across between data centers. Very few companies can cover all of that with their own silicon and optics.

Second, AI infrastructure demand is spreading beyond the hyperscalers.

Sovereign clouds, neoclouds, and many enterprise customers often lack the capability to design and operate AI data center networks the way AWS or Azure does. That drives growing demand for a validated turnkey stack where chips, systems, networking, optics, security, and operational tooling come bundled together. As geopolitical tension increases, sovereign AI infrastructure demand at the national level only gets stronger.

In this environment, Cisco offers a full-stack AI infrastructure proposition built around networking and security.

2. Is Demand Actually There?

Good technology that doesn’t sell doesn’t matter. So let’s start with whether it’s selling.

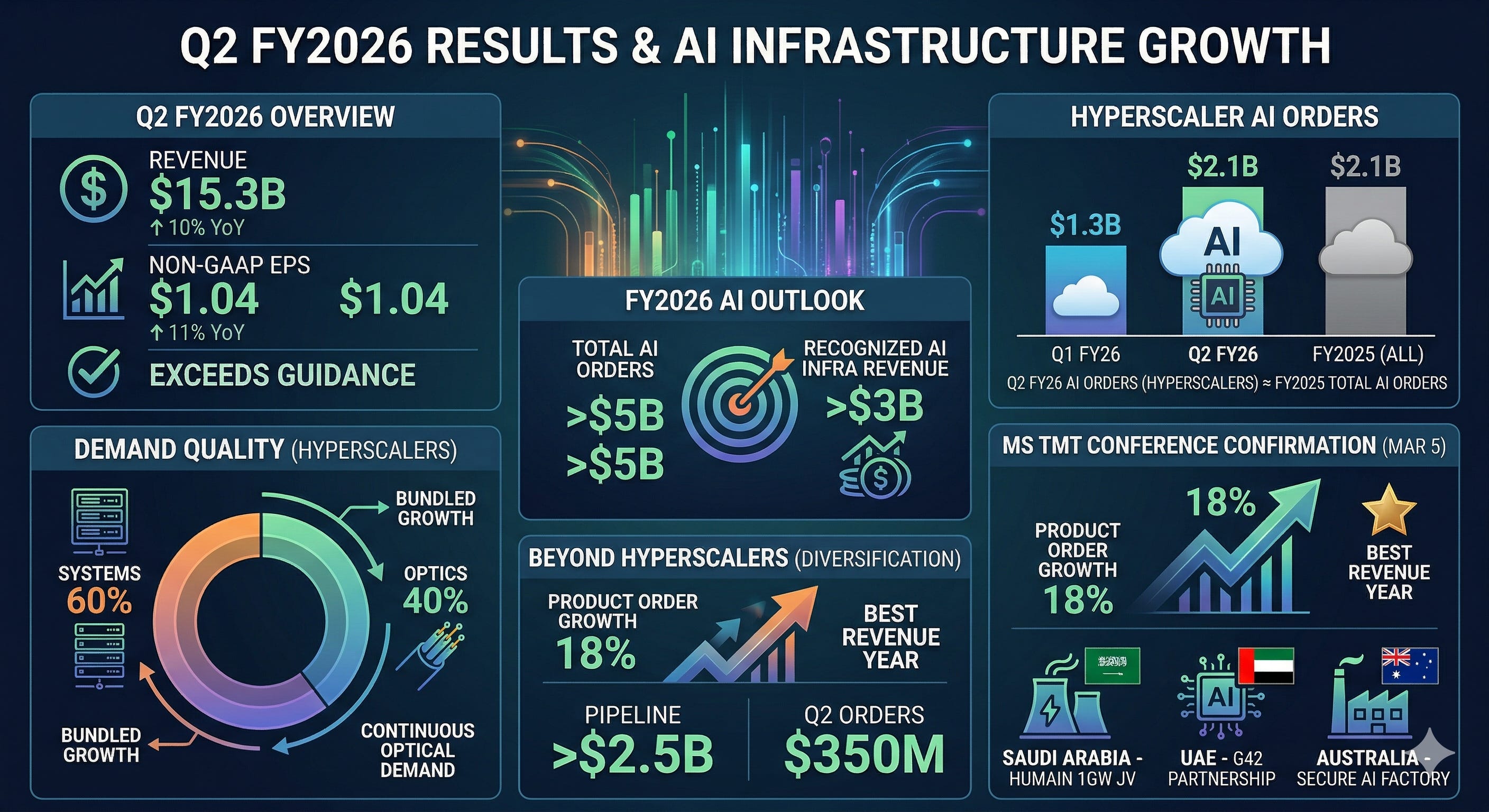

Q2 FY2026 results, reported February 11

Revenue of $15.3B, up 10% year over year. Non-GAAP EPS of $1.04, up 11%. Both came in above the high end of guidance.

AI infrastructure orders from hyperscalers alone hit $2.1B in a single quarter, up sharply from $1.3B the prior quarter and roughly equal to all of FY2025’s AI orders combined. The company is guiding for total AI orders to exceed $5B in FY2026, with recognized AI infrastructure revenue exceeding $3B.

The composition of demand is worth noting. Hyperscaler AI infrastructure revenue runs roughly 60% systems, 40% optics. This isn’t a one-and-done switch sale. The optical connectivity demand that follows keeps regenerating. Systems and optics grow together in a bundled structure. At the Morgan Stanley TMT Conference on March 5, management confirmed product order growth accelerating at 18% and projected this to be the best revenue year in company history.

Beyond the hyperscalers, sovereign and enterprise momentum is real. The neocloud, sovereign, and enterprise pipeline is above $2.5B, with $350M in orders from that segment in Q2 alone. Saudi Arabia’s HUMAIN 1GW AI infrastructure JV, the UAE G42 partnership, and Australia’s Secure AI Factory are concrete examples.

I want to add a personal experience here.

Recently, a hiring manager from Cisco’s Silicon One team reached out to me directly and asked whether I would be interested in interviewing. Silicon One is Cisco’s in house networking ASIC family. It is the core silicon behind Cisco’s AI infrastructure strategy, designed to unify routers, switches, and service provider equipment under a single chip architecture.

Anyone who has prepared for a job move in the United States will know that it is actually quite rare for a hiring manager to contact you directly. That was exactly why I became curious and decided to take a short call. During that conversation, I heard several things that left a strong impression on me.

What came through was clear. This team is scaling up in a serious way. They are actively recruiting semiconductor engineers across Silicon Valley. There is a multi generation roadmap behind this effort, and they are building the organization with the intention of sustaining it over time. My impression was that Cisco is not treating this as a side project or a short term push. They appear to be in a phase of real internal expansion.

After that call, I went back and re examined Cisco’s public data from the ground up. And I came to the conclusion that the market is still missing something. A detailed breakdown of Cisco’s technical moat follows in the next section.