Sivers Semiconductors: Verifying the Thesis After a 2,100% Run in Six Months

A small-cap with direct exposure to the laser source bottleneck of the CPO era. Can it go further from here?

Over the past six months, Sivers Semiconductors has risen 2,104.31%.

As of May 26, 2026, SIVE.ST closed at SEK 86.85.

A move like this splits the market into two camps.

One side sees it this way.

“A money-losing company doing SEK 306.6M in revenue, roughly $33M, has climbed to a market cap above $2.5B. That puts trailing P/S around 80x. There were financial restatements during PCAOB alignment, and there are allegations of information leakage ahead of the potential Nasdaq dual listing announcement. This is an overheated small-cap riding the AI and CPO narrative.”

The other side sees it differently.

“Sivers is not just another optical component company. As AI datacenter networks move past 800G and 1.6T pluggables toward CPO and external light source architectures, the industry will need multi-wavelength laser sources that can deliver stable output across multiple wavelengths. For Sivers, this market could be the inflection point that transforms the entire revenue structure.”

The honest assessment: yes, the stock is expensive at current prices.

A money-losing company trading above $2.5B in market cap.

But dismissing it purely on valuation means ignoring customer engagement and a technology position that are hard to wave away.

So this article looks at three things.

First, where exactly Sivers sits in the technology stack.

Second, which of the publicly known customer engagements are confirmed and which are inference.

Third, if those engagements convert to production revenue, how far the current market cap can be justified.

The goal is not to declare Sivers good or bad. It is to map out what production success the market has already priced in, which signals should trigger a re-examination of the thesis, and how to think about and approach this stock as an investment.

Table of Contents

Why the Market Started Seeing Sivers Differently

Types of Lasers and What Sivers Makes

Competitive Landscape and Sivers’ Positioning

Who Is Buying: Customer Mapping

Financial Reality: Losses, Cash Burn, Runway

Valuation: What the Current Price Already Reflects

What Would Make Me Wrong

Investment View and the May 29 Checklist

Disclaimer

This article does not recommend buying or selling any security. All analysis, opinions, and scenarios are based on publicly available information and the author’s interpretation, and should not be construed as investment advice. While the technical analysis of the semiconductor and optical component industry reflects the author’s industry experience, the financial analysis and valuation scenarios are assumption-based estimates. Sivers Semiconductors is a Swedish-listed small-cap with limited liquidity, a pre-production money-losing company with extreme price volatility. This article was written as of May 27, 2026, and conditions may change after the Q1 2026 earnings release on May 29. Investment decisions are entirely the reader’s own responsibility.

1. Why the Market Started Seeing Sivers Differently

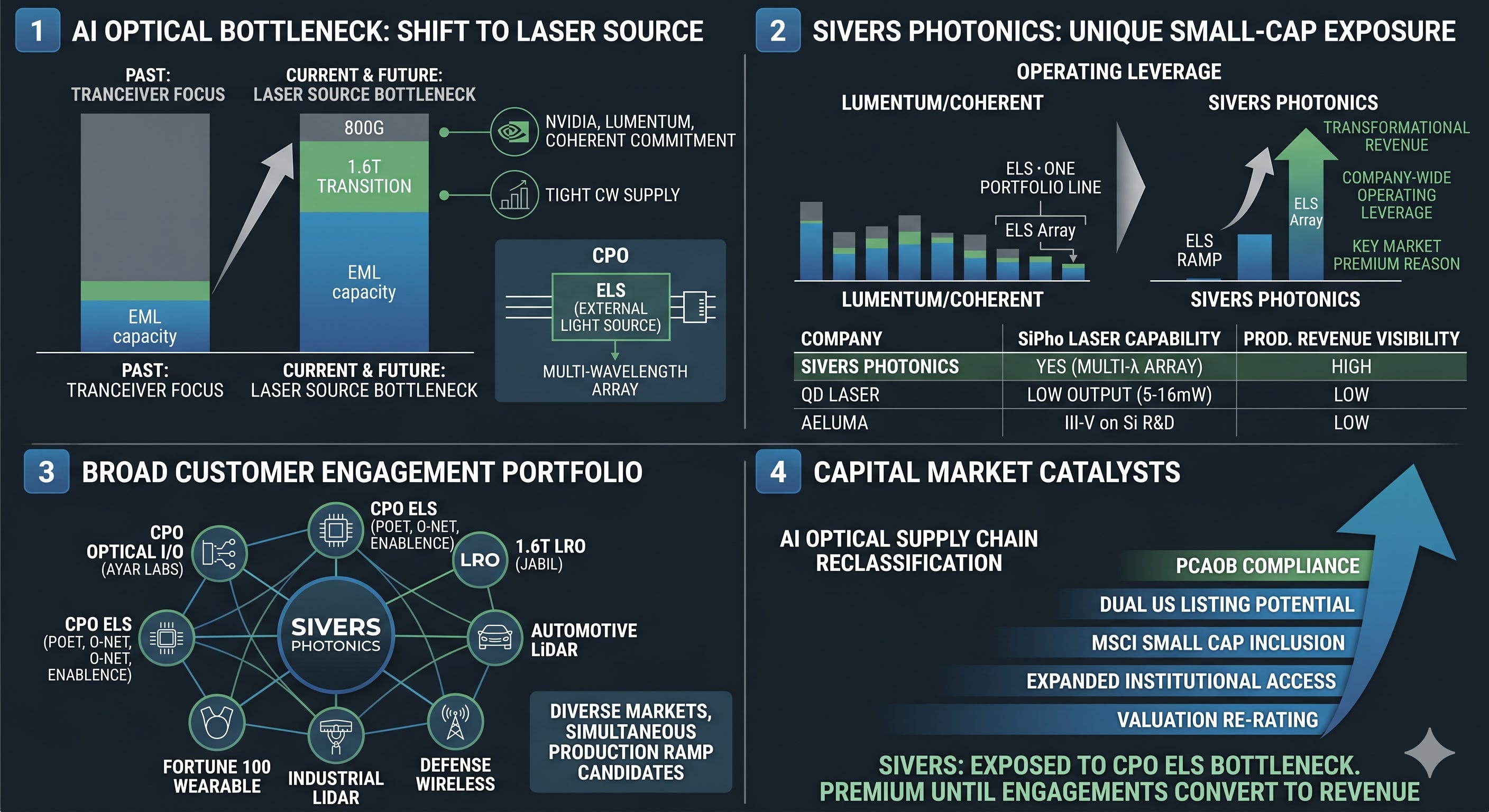

The market began assigning a premium to Sivers because four shifts converged at the same time.

First, the AI optical bottleneck narrowed from transceivers broadly to laser sources specifically.

In the 800G and 1.6T transition, EML capacity is already tightly locked in along the NVIDIA-Lumentum-Coherent axis. NVIDIA secured multi-billion purchase commitments with Lumentum and Coherent, and merchant CW supply is getting tight.

With CPO, lasers cannot go inside the GPU package, which means External Light Sources (ELS) are needed. Among several approaches to building an ELS light source, one is a multi-wavelength array that delivers multiple wavelengths simultaneously from a single source. What the market has started paying attention to is not “optical growth” in general, but “laser source scarcity in the CPO era.”

Second, Sivers is a public small-cap with direct exposure to that scarcity.

Lumentum and Coherent can build array light sources, but for those companies, an ELS array is one line inside a massive portfolio. For Sivers at a $2.5B market cap, the same ELS ramp is an inflection point that transforms the entire revenue structure. This difference in operating leverage is the fundamental reason the market assigns Sivers a separate premium.

Even among SiPho light source small-caps, the distance to production varies widely.

QD Laser (TYO: 6613) outputs 5 to 16mW per channel, which has not been enough to secure a CPO ELS production customer.

Aeluma (NASDAQ: ALMU) takes an interesting long-term approach by growing III-V directly on Si, but FY26 Q3 revenue of $1.2M came mainly from R&D contracts, and the path to production revenue is less visible than Sivers.

Among this group, Sivers is closest to production revenue conversion.

Third, the breadth of customer engagement changed completely.

Ayar Labs (CPO optical I/O), POET (CPO ELS), O-Net + Enablence (CPO ELS module), Jabil (1.6T pluggable LRO), a strategic LiDAR customer (automotive and industrial), and a Fortune 100 wearable customer all showed up across different markets simultaneously.

This is not a single speculative CPO bet. CPO, pluggable, LiDAR, wearable, and defense wireless are stacking up as production candidates at the same time.

Fourth, capital market catalysts layered on top of technology catalysts.

PCAOB alignment, a potential US dual listing, MSCI Small Cap inclusion, and an expanded share base after directed share issues all point in the same direction. The market is beginning to reclassify Sivers from a small Swedish photonics company into a public vehicle that could be integrated into the AI optical supply chain.

If the US dual listing goes through, it opens access for US institutional investors and becomes a catalyst for valuation re-rating.

Sivers is not getting special treatment because it is the best laser company.

It is getting attention because it is one of the public small-caps with direct exposure to the external laser source bottleneck of the CPO era. But this premium only holds if the announced engagements convert to actual production revenue.

2. Types of Lasers and What Sivers Makes

Three Categories of Datacenter Light Sources

InP-based laser sources used in datacenter optical communications fall into three broad categories.

EML (Electro-absorption Modulated Laser). A device that combines the light source and modulator into one component. It is the primary light source for 800G and 1.6T pluggable transceivers, with Lumentum, Coherent, and Japanese IDMs as the main suppliers. Currently the largest revenue category in AI datacenter optical interconnects.

Single CW DFB. A continuous-wave laser that only emits light, with no modulation. Used as an external light source for silicon photonics transceivers. Lumentum and Coherent are also the main suppliers here. Lumentum announced UHP 400mW (launched in 2025) and has shown its 800mW SHP roadmap. Coherent unveiled a 400mW CW at ECOC 2025.

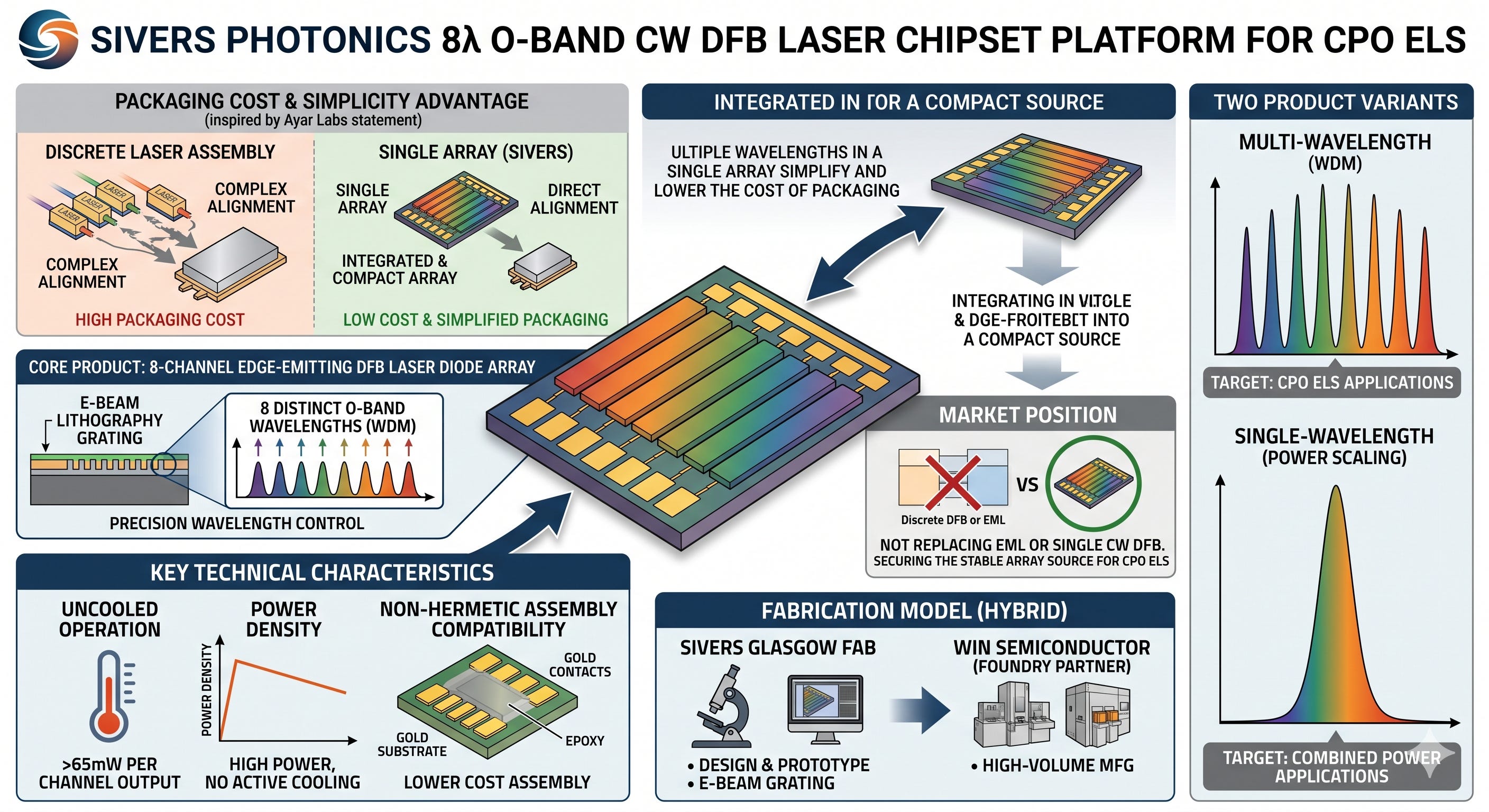

Multi-wavelength DFB array. A structure that delivers CW laser output at multiple wavelengths simultaneously from a single source. When the industry transitions to CPO (Co-Packaged Optics), an External Light Source (ELS) module is needed next to the GPU or switch package. There are several approaches to building an ELS light source: placing discrete single-wavelength CW lasers for each channel, splitting a single high-power CW output through a splitter, or using a multi-wavelength array that delivers multiple wavelengths from a single source simultaneously.

Sivers fits into the multi-wavelength array approach.

What Sivers Makes

The core product from Sivers Photonics is the 8-lambda O-band CW DFB Laser Chipset. The official description: “8-channel edge-emitting high-power DFB laser diode array designed for CW use in WDM applications.”

Delivering multiple wavelengths from a single array is the core of this product. Ayar Labs states directly in its SuperNova light source description that “multiple wavelengths in a single array simplify and lower the cost of packaging.”

The logic: instead of assembling discrete lasers and aligning them inside a module, having multiple wavelengths from a single array simplifies packaging and reduces cost.

The chipset platform offers two variants. A multi-wavelength variant where each channel outputs a different wavelength (for WDM), and a single wavelength variant where all channels output the same wavelength (for power combining). The multi-wavelength variant is where the CPO ELS thesis concentrates.

Key technical characteristics include e-beam lithography-based DFB grating (precise per-channel wavelength control), uncooled operation (65mW+ per channel without active cooling), and non-hermetic assembly compatibility (packaging cost reduction). Sivers runs a hybrid model: design and prototyping at its own Glasgow fab, with high-volume production outsourced to WIN Semiconductor.

Sivers is not competing with EML, and it is not in an output competition with single CW DFBs. It targets the ELS array position where multiple wavelengths need to be delivered reliably from a compact source.